Landfill Gas-to-Renewable gas production is set to more than double by 2030, but project success depends on location and scale according to Wood Mackenzie

Press Release

Landfill gas remains the most popular feedstock option for renewable gas production (LFG-to-RNG), but project pre-tax breakeven prices can range, with success relying heavily on location and scale, according to a new report from Wood Mackenzie.

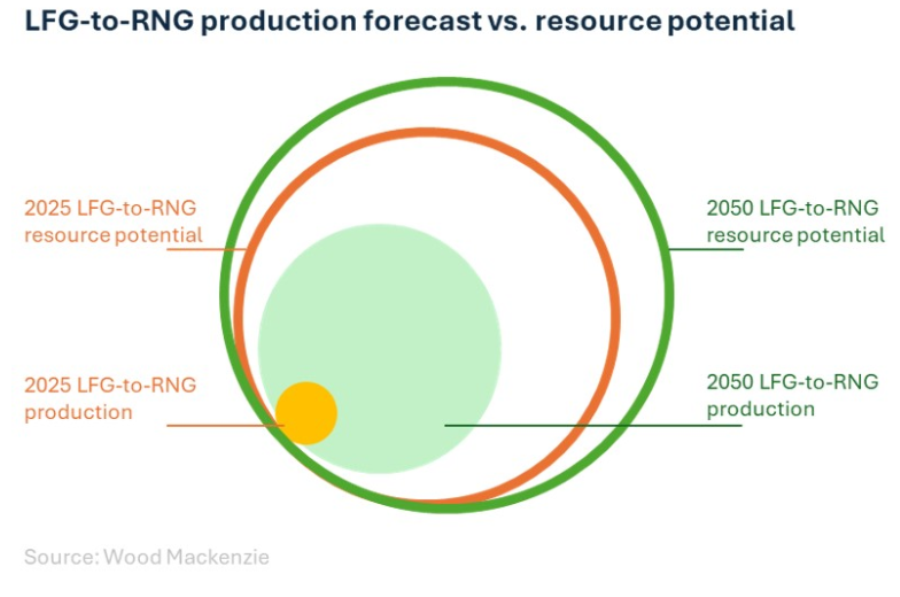

In the report “Trashing your way to a cleaner future: landfill gas as a feedstock for RNG in North America” Wood Mackenzie finds that LFG-to-RNG capacity has nearly doubled in the last five years, and the prospect for more activity is considerable, with only 10% of the resource potential currently being utilized in North America.

“The LFG-to-RNG sector has been extremely active in the last two years with new project ramp-ups, blockbuster M&A deals and new players entering the market,” said Dulles Wang, director of research at Wood Mackenzie. “The sector is also consolidating, with the top seven developers making up more than 60% of the market today. As RNG is a direct substitute for fossil-based natural gas, there is tremendous potential for future growth and its prospects in carbon reduction goals.”

According to the report, four main factors contribute to the ultimate success of an LFG-to-RNG project, which include:

Economies of scale: Economies of scale have the largest impact on project costs, as studies have noted a stronger correlation between cost and scale than cost and upgrader technology type.

Location: An RNG upgrader’s proximity to a landfill has the largest impact on the interconnection costs and states with more stringent environmental regulations can increase costs as well.

Upgrader technology: Capital costs for upgraders can vary based on technology type.

Operational efficiency: Operating costs can range from 3% to over 60% of capital costs, with a significant portion coming from utility costs.

“When factoring all of these drivers into play, making an LFG-to-RNG project work requires collaboration between landfill owners and RNG developers, and costs vary significantly from project to project,” said Wang. “Despite cost variations, LFG-to-RNG is the lowest-cost option for RNG production, and the subsidy value of RNG could reach over US$20/mmbtu when considering stacking of different Environmental Attributes.”

According to the report, currently RNG pre-tax breakeven price ranges from US$4 to US$35/mmbtu, with an average of US$15/mmbtu.

Market poised for growth

Wood Mackenzie forecasts that the resource potential could exceed 5 billion cubic feet per day (bcfd) by 2050, up from less than 4 bcfd today, and that production could reach 2.2 bcfd by 2050, up from .3 bcfd today.

“With population growth, we expect more landfills,” said Wang. “Landfills are one of the largest sources of methane and increased scrutiny by governments on methane regulation will likely boost more LFG-to-RNG conversions. Not to mention, policy incentives have targeted the RNG industry as demand for it rises – especially in the transport sector. The relatively lower carbon intensity (CI) of the LFG-to-RNG process on a life-cycle basis compared to conventionally produced natural gas provides the economic justification for the subsidies. we expect more LFG-to-RNG projects to take off due to attractive economics.”

Wang notes that challenges still exist, such as the relatively high CI compared to other RNG technologies potentially driving investors away as they seek higher returns from subsidies. Challenging economics for small-scale or more remote projects may also hinder the pace of long-term project development as costs rise for second tier resources, while inflationary pressures in recent years may affect cost breakevens structurally.

“Despite some challenges and unknowns, we see a bright future for LFG-to-RNG,” said Wang. “RNG will play an increasing role in decarbonizing North American economies, and with LFG-to-RNG capacity nearly doubling in the last five years, we expect the trend to continue in the foreseeable future.”